Our accountants in Italy can help foreign investors who want to open companies and can offer tax advice together with a wide range of financial services.

| Quick Facts | |

|---|---|

| Who requires accounting services in Italy |

Resident and non-resident companies with activities in Italy |

|

Applicable accounting legislation |

– Italian Civil Code, – International Financial Reporting Standards (IFRS) |

|

Types of accounting services we offer |

– bookkeeping, – payroll, – annual financial statements, – tax returns, – debt monitoring |

| Tax advice and compliance (YES/NO) | Yes |

| We offer support for tax registration |

Yes |

| Financial planning for company owners | We offer dedicated financial plans on request |

| Risk assessment and evaluation |

Offered after company registration in Italy |

| Types of audit services |

– internal, – external, – financial, – compliance, – operational |

| Tax minimization methods available |

– tax credit planning, – charities, – retirement plans, – selling investments that lost their value |

| Personalized financial consultancy services | On request |

| Investment consultancy for high-net-worth individuals |

Dedicated plans on request |

| Financial and analysis reports for companies |

If solicited |

| Human resources services available (YES/NO) |

Yes |

| Expertise provided by certified accountants (YES/NO) |

Yes |

| Free case evaluation for companies (YES/NO) |

Yes |

Table of Contents

What are the accounting services we offer in Italy?

The following accounting services are available with our accountants in Italy:

- accounts payable and receivable;

- tax and VAT registration;

- preparing and filing financial statements;

- payroll;

- audit services;

- bookkeeping services.

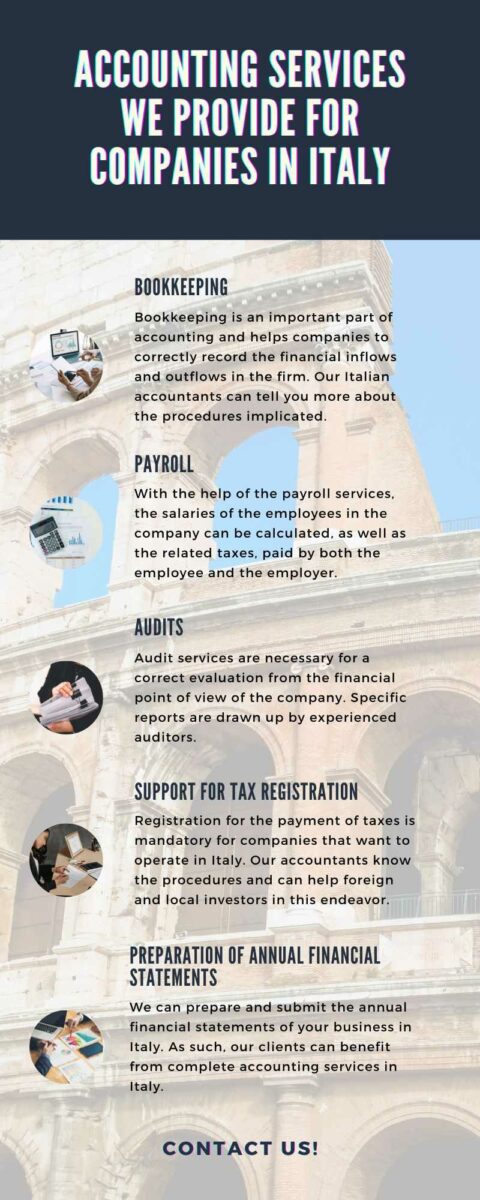

Our services are oriented towards both small and medium-sized enterprises (SMEs), plus large companies in Italy, so feel free to ask about accounting in Italy. You can also read the following infographic:

Bookkeeping services in Italy

Our team of accountants in Italy can provide bookkeeping services for your company. This kind of process implies a series of tasks related to the control of payable and receivable accounts of a firm operating in Italy. Banking operations, cash management, invoice issuance, and effecting payroll are essential bookkeeping tasks. The accountant in Italy who works for your business is in charge of all financial activities, including the ones related to income statements, petty cash books, daybooks, and journals. Bookkeeping is an essential part of the accounting services we provide to our customers in Italy.

If you are interested in hiring the services of our accounting firm in Italy, please feel free to discuss with one of our specialists and find out all you need to know about how to control the finances of your firm. We are here to provide complete support for your company in Italy, right from the start.

Tax minimization options for your company in Italy

Entrepreneurs are always interested in cutting the amount of taxes that need to be paid in their firms. This is where tax minimization instruments can be adopted, with the help of our accountants in Italy. An important method to cut down the amount of taxes is to make credit payments in advance. Having a charity or donation organization is also a great solution that can be explained by one of our specialists. Also, you can consider a retirement plan or the taxes for bonuses and office supplies that can be eliminated.

One should note that tax minimization tools will be implemented after a serious and accurate verification of the financial aspects of a company in Italy made by one of our specialists. Our experts can offer a series of solutions tailored to the business needs of the company owner.

Would you like to set up a business in Italy? With 1 Euro as minimum share capital, you can register an SRL in this country, the most accessible structure available. In this sense, a bank account and a business license will be needed, depending on the activities undertaken. Our local agents are at your disposal with the necessary assistance and services to be able to start the activities as quickly as possible. Contact us for a personalized offer.

Below you can watch a video presentation we have prepared on this topic:

Our company offers audit services in Italy

Our accounting team in Italy provides services for the restatement of annual accounts in accordance with the International Financial Reporting Standards (IFRS) applicable in Italy. In addition, for the fulfillment of these standards, our accountants plan and perform the audit in Italy in order to obtain reasonable assurance about whether the financial statements are free of material misstatement. The audit services we provide in Italy contain examining, on a test basis, of evidence supporting the disclosures in the financial statements.

Furthermore, our Italian audit services include assessing the accounting principles used and significant estimates made by the management, as well as evaluating the overall financial statement presentation.

Our accounting firm will also prepare the cash flow, revenue, and expenses, as well as the required documentation for obtaining loans.

Are payroll services of interest to your company?

If you are in need of payroll services, our Italian accountants will make sure that all procedures for the preparation of payrolls, as well as establishing liabilities in relation to wages, are made accordingly. These services are extremely important to companies with operations in Italy and involve a wide variety of tasks, like the distribution of electronic payroll records, salary calculation, payroll tax calculation, to give a few examples.

Those interested in complete accounting in Italy for their companies can solicit our help instead of creating an entire accounting department. Also, if you are for the first time in Italy and need assistance in company formation, talk to our specialists and solicit guidance and assistance.

Assistance in the double taxation issue

Double taxation is a main issue when it comes to business anywhere in the world. As such, any foreign investor who runs a business in Italy should be aware of the double tax treaties signed between Italy and other countries. As the main purpose of such treaties is to avoid tax payment in Italy and in other countries, we advise you to work with our Italian accountants to get full assistance and representation.

Do you need a loan to sustain your business?

We know very well how important it is to obtain a loan in order to sustain your business in Italy, but we also know the difficulties one can encounter when applying for a loan. Having experience in this matter, we can provide specific information about the Italian banking system, so you will be up to date with all the rulings and regulations adopted by the bank institutions you are working with. In addition, you will have access to all the information available regarding European Funds, including for the new European Program for the period 2014-2020 allocated for Italy.

Attributes of a chartered accountant in Italy

A chartered accountant in Italy has specific accreditations and specialized studies in this area, as well as vast experience. In addition to normal accounting services dedicated to companies or sole traders, a chartered accountant can be involved in forensic accounting for situations of commercial fraud or litigation. A chartered accountant in Italy can also offer specialized advice and personal financial opinions for high-net-worth individuals and company owners. The way the funds can be managed in a business also comes to the attention of such an accountant in Italy.

In criminal cases related to business and fraud, a chartered accountant in Italy can offer his expertise in the field, thanks to the experience gained over the years. If you also need the services of such accountants in Italy, we invite you to get in touch with our local specialists. You can benefit from personalized services for the company you own and not only.

Publication requirements in Italy

Companies with activities in Italy must comply with the accounting standards imposed by the Italian Accounting Organization. Among them are publication requirements. Audit reports, financial statements, and other annual reports are prepared. There are exceptions, however, and these refer to unlimited liability companies that must only present a balance sheet of profits and losses. Also, in the case of companies listed on the stock exchange, they have the obligation to present financial statements quarterly.

Audit committee for LLCs in Italy

Limited liability companies in Italy that have a capital exceeding EUR 120,000 must appoint an audit committee for 3 years or more. They are in charge of annual audits and the reports involved in order to produce annual financial statements.

But as regards the companies listed on the stock exchange, such firms must be audited by a group of independent and external auditors.

Our accountants in Italy can explain the audit process for small, medium, and medium-sized companies.

We offer competent advice in company management and business development

The most important step in running a business efficiently is to have a great management strategy. If you want to climb up to a top position on the Italian market, contact our team of specialists in management and business development.

You will benefit from customized management strategies that will improve your company’s financial results and will strengthen your company’s position among competitors. We remind you that our company registration consultants in Italy can also assist in registering a business in this country.

What are the benefits our company brings?

Our team is made of chartered accountants and human resources inspectors. Our accountants will help you with preparing the monthly trial balance and preparing and depositing the annual financial statements. Our Italian accountants will also establish the monthly and quarterly payment obligations, prepare documents for payment, and calculate the taxes you have to pay to the Italian authorities.

The Italian taxation system

Moving to Italy implies paying the income tax which is applied progressively at rates ranging between 23 and 43%. In the case of companies, the corporate tax in levied at a 24% rate for businesses registered here. However, tax deductions and allowances are available for individuals. In the case of companies, there are various tax minimization solutions available, such as tax deductions and reliefs. Also, the government has created several incentives for companies which can go up to 200,000 euros over a period of 3 years. It should be noted that the financial year in Italy starts on January, 1st and ends on December, 31st. The following documents must be filed at the end of the financial year by Italian companies:

- an annual financial report;

- audited financial statements;

- a balance sheet;

- a profit and loss account.

It must be noted that not all the documents listed above must be filed by small companies. These can submit shorter forms of the financial statements. Large companies must also file a copy of the annual general meeting of the shareholders.

What is forensic accounting?

In the situation in which a foreign investor entered into a conflict with another business partner and the case has to be brought to the Italian court, it is necessary to perform forensic accounting if the company’s files are the subject of the case. Forensic accounting combines accounting and audit techniques with investigative techniques, applicable to the company’s financial statements. After the extensive and detailed analysis is completed, the investor can use the results in court.

The investigation is usually carried out by a forensic accountant, a person familiar with the accounting and financial systems applicable in Italy. The forensic investigation is performed in such a manner that it can offer plausible answers to various issues that were brought in front of the court. This technique can be used for many legal problems, such as fraud or embezzlement; our team of Italian lawyers can offer more details on this matter.

The attributes of a forensic accountant in Italy

When hiring a specialist to perform forensic accounting on the financial statements of the company, the investor should expect that he or she will perform the following tasks:

- analyzing the company’s documents in order to investigate flaws or hidden financial activities;

- developing computer presentations which will be used when presenting the results of the investigation;

- setting up a report comprising all the findings (that have to be backed up by specific documents);

- participating in the legal proceedings;

- testifying in the court;

- preparing visual aids.

Other tasks that enter the attention of an accountant

Accountants in Italy can also be involved in mergers & acquisitions and tax planning. Those interested in M&A can ask for specialized help in order to be sure that the process will be fair and uncomplicated. You can also ask for advice on company restructuring, liquidation, or relocation if you have such plans.

Why choose outsourcing accounting in Italy?

Choosing an accounting firm in Italy to deal with these aspects is an advantage for a company. Instead of an entire department taking care of the company’s accounting, it is much more advisable to call on an experienced team. In addition to knowledge in the field, you can also benefit from advantageous costs for the services offered, and these are calculated according to the number of employees, the type of company, activities, responsibilities, etc.

If you want to know more about the advantages of outsourced accounting services, please contact our specialists.

Why work with our team of accountants in Italy?

Our company has gathered an accounting team in Italy in order to provide services tailored according to your needs. We offer services in financial accounting, fiscal and human resources. Our accountants in Italy will be at your service if you need assistance in financial and management accounting, tax consultancy, payroll, personnel administration, and, of course, consultancy on management accounting. Ask us anything about accounting in Italy.

FAQ about accounting in Italy

1. Why should I externalize the accounting in Italy?

Hiring the services of an accountant in Italy is essential to the company’s business direction. Transparent, efficient, and professional services can be offered by our team of accountants in Italy.

2. Do I receive payroll and bookkeeping services in Italy?

Yes, payroll and bookkeeping are essential parts of accounting in Italy and are comprised of the package we can offer. We have a team specialized in these matters, so feel free to talk to us.

3. Can I ask for help with tax registration in Italy?

Yes, it is important to properly register the company for taxation in Italy, a matter where our specialists can provide help and guidance. We work closely with the authorities in charge of tax registration.

4. Can I get advice for annual financial statements?

Yes, the annual financial statements are important documents in the firm. These are normally submitted at the end of the year, helped by one of our accounting specialists in Italy.

5. Why hire our accounting services in Italy?

We have a team of professional accountants in Italy, ready to take care of all the financial aspects of your company. Our experts are Certified Public Accountants and registered with the International Federation of Accountants. Feel free to discuss any accounting aspect that might concern you and let us explain all the services we can provide for your company in Italy.

We have gathered some facts and figures about the economy and business direction in Italy that you might find it useful:

- More than USD 454 billion was the total FDI stock registered in Italy in 2021.

- The USA, France, Germany, and the UK remain the main investors in Italy.

- The 2020 Doing Business report issued by the World Bank ranked Italy 58th out of 190 economies in the world.

- Around USD 7 billion was the total value of the greenfield investment registered in Italy in 2019.

- Most of the foreign investments in Italy are directed to sectors like manufacturing, retail trade, wholesale, financial, and insurance activities.

If you are interested in accounting services in Italy and other European countries, such as Bulgaria or Turkey, you can contact us. Also, if you want to register a company in Italy, do not hesitate to discuss it with us. If you need accounting services in Croatia or other countries, we can put you in touch with our local partners.